Compliance is a Negotiation

Compliance is a Negotiation

Legal as a Product, Compliance as a journey, and John Travolta as Robert Shapiro

Welcome to another edition of IF:Then: a venture community of attorneys and regulatory experts that helps founders and startups navigate challenging and emerging regulatory environments.

If you are you in legal, regulatory, government affairs, or compliance and interested in joining the IF:Then community please reach out to me at david@ifthen.vc

If you are a founder/startup looking for help with regulatory strategy or product development, then email contact@ifthen.vc

And of course if you’re reading this and want to continue to get more discussion and analysis at the intersection of law and technology, hit the button. Let’s go!

At IF:Then, we can and will support any startup where navigating legal and compliance is critical to their product development, customer acquisition, growth, and overall success. Innovators in cannabis, crypto, gaming, and other emerging industries fit naturally, given that they operate in what are simultaneously (and somewhat ironically) heavily regulated yet uncertain regulatory fields. From a broader perspective, nearly any Fintech is aligned as well. Many of the innovations in venture’s hottest sector that have changed how we bank, move money, and invest stem directly from product features and experiences that pushed the envelope faster than regulators could keep up.

However, where IF:Then will look to make the biggest bets as investors, and where we can likely best see the field and add the most value, is with companies that create new opportunities and expand markets by transforming legal instruments or regulatory concepts into their product.

The simplest version of Legal as a Product (“LaaP”: I think it works!) disintermediates the traditional law firm structure and streamlines common documentation and services. Think LegalZoom ($7.5B IPO earlier this month) or Rocket Lawyer (raised $223 million this year). Valuable businesses, but more law than tech.

Another version of LaaP consists of compliance-focused products streamlining aspects of KYC (know your customer) and AML (anti-money laundering) such as identity verification, transaction monitoring, onboarding, background checks or sanctions review. These companies address a market of banks, Fintechs, and marketplaces in regulated spaces. They have done a lot for back-office efficiency and significantly improved user experiences, and there’s still plenty of room for innovation but its largely compliance for an existing market.

The most dynamic side of LaaP is with companies that create and expand their own markets. By removing friction around and increasing access to a legal instrument or concept, they are creating opportunity for expansion. Sometimes creating that opportunity is as simple as making people aware of a legal concept — “hey did you know this was a thing?” — and putting a nice product experience around that.

More companies are at least partially based on this concept than you might think, and they generally don’t come across as “legal” focused. Main Street ($60m Series A) can find a startup or small business tax credits that are apparently just sitting right there for the taking. Free money! Fifteen years ago this business would have been positioned like a J.G. Wentworth Ad (“They’re my tax credits, and I want them now!”), but instead it’s built as a Fintech product, a 0% APR cash advance for any credits they find, an integration with your payroll provider, and a dashboard for how much money they’ve saved you. But behind the scenes, the core of this business is tax law and paperwork.

Remote, Deel, and Panther streamline the many complications with hiring a global workforce including payroll, compliance, taxation. Each of them is putting a nice product experience around legal paperwork, and reducing the otherwise complicated friction of having the employee set up an LLC for you to pay as a 1099 contractor.

These companies aren’t making it easier to comply with regulations, they’re providing access to what is possible. They’re letting unknowing businesses know these tax credits are available to them, and giving startups that otherwise wouldn’t have the confidence to hire around world.

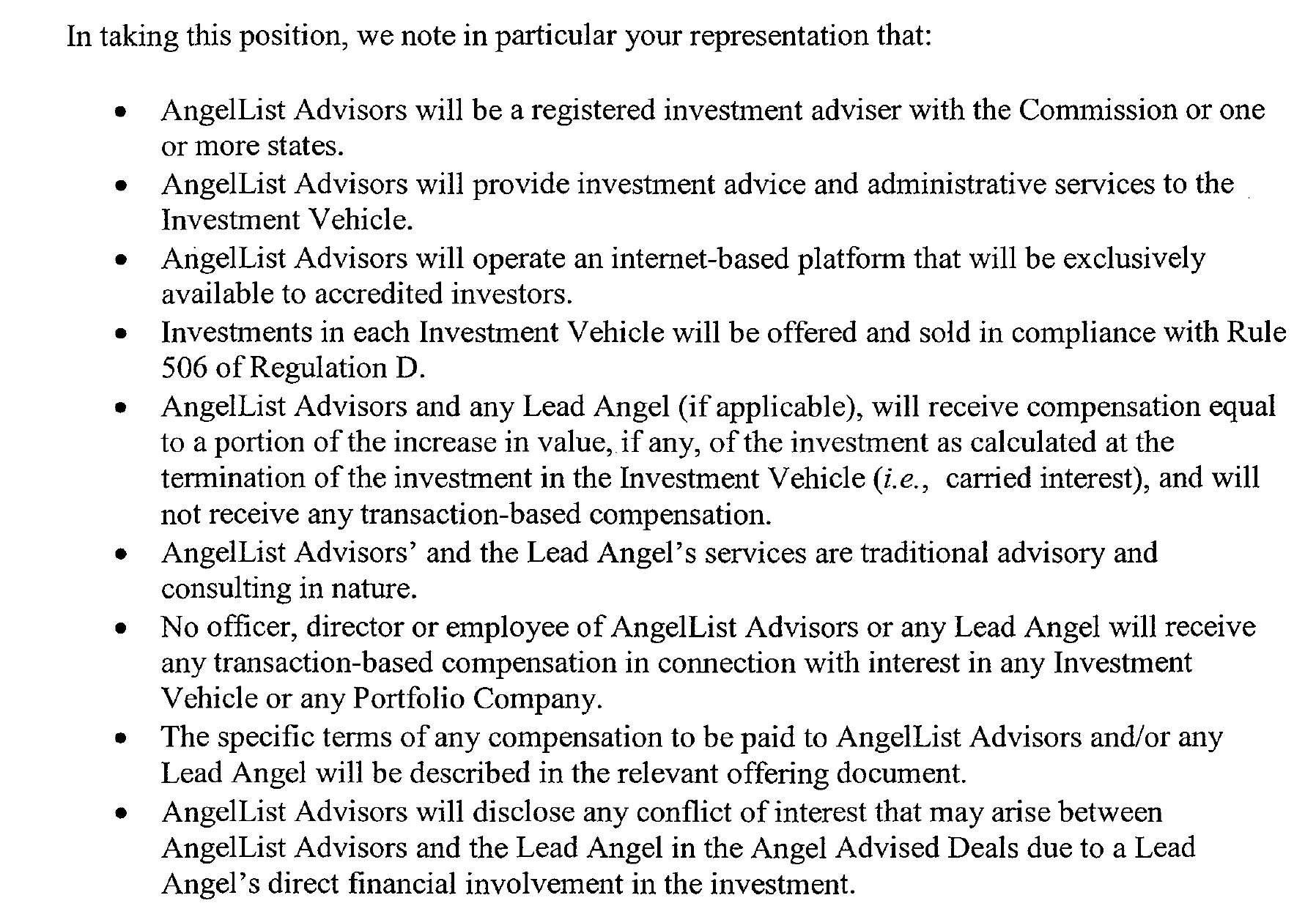

Perhaps no company embodies LaaP more than AngelList. That you are reading this right now owes a lot to AngelList and the productization of a well-worn legal instrument — the Special Purpose Vehicle (“SPV”). Syndicates are hardly new, and AngelList isn’t even the first company to productize the SPV. AngelList started in 2010 as something of a matching tool, riding the crowdfunding wave popularized by Indiegogo and Kickstarter, but bringing the idea to venture startups and providing a technology layer and marketplace for existing VCs and accredited investors. A huge catalyst came later, in 2013 when it and FundersClub received no-action letters from the SEC for their proposed syndicate and advisory platform. The SEC letter laid out the various regulatory hurdles that AngelList’s plan had ostensibly cleared, and the guardrails for how to operate going forward:

Receiving this letter, and the corresponding green light that accelerated the business, was the result of well-thought-out legal strategy. They presented a fully baked product to the SEC complete with details around corporate structure, platform services, flow of funds, and regulatory compliance. AngelList founder Naval Ravikant’s quote to Techcrunch brings the idea home:

“It lets us know the legal boundaries of what’s possible in the space and will inform our future products”.

What’s key here is the part where he mentions the products. Clearing the legal hurdle of the instrument is just step 1 — there’s a reason this article is about AngelList and not FundersClub. The product’s the thing. The legal instrument is the jumping-off point. AngelList productized the SPV (and subsequently the Rolling Fund, and the Roll-Up vehicle) realizing the opportunity to expand its reach beyond existing VCs and Naval’s buddies.

Yes, with a productized SPV, any idiot with a Substack, a thesis statement, a few dozen accredited friends, and a willingness to fire off twitter DMs can start their own syndicate. But the real value is that AngelList created the opportunity for anyone (accredited) to theoretically start from zero. To source LPs through the platform, to build a brand entirely within the platform, to get accredited investor confirmation, take care of tax filings and blue sky laws, and comply with various SEC regs directly through the product flow. Add in embedded payments, a social component, and the ability for LPs to join any number of syndicates and track their investments, and you’ve hit the buzzword-before-it-was-a-buzzword jackpot to “democratize” angel investing.

For IF:Then, identifying these concepts and seeing the opportunities will be our wedge, and helping founders realize and capture those opportunities will be a key part of our execution. These are unique businesses and concepts, but we are uniquely positioned to help bring these visions to fruition.

Stump the Schwab

Brokerage preparing for $200m SEC fine

You have to at least hand it to brokerage giant Charles Schwab, they don’t act first, but they do act eventually. They rolled out zero-cost trading in response to Robinhood. They rolled out robo-advising in response to Wealthfront and Betterment. Unfortunately their refusal to be left behind apparently extends to robo-related fines from the SEC, because this week Schwab said in a regulatory filing that it is booking a $200m charge pursuant to an SEC investigation of its “historic disclosures” related to its robo-advisor platform.

It’s not clear yet where Schwab went wrong, but in 2018, Wealthfront got stung for $250,000 for a lack of proper disclosures, some misleading statements, and some bad tweets. $200m is quite the step up from$250k so maybe Schwab has been lying to consumers and poorly executing the Anakin/Padme meme.

As robo-advising continues to expand, and the broader concept of self-driving money cements itself, platforms are going to have to remember that the more they remove humans from the process, the more important it will be for product flows to provide appropriate disclosures beyond clickwrap agreements and hidden provisions in your terms of service.

Same Shit Different “Banks”

Chime and Wells Fargo Closing Accounts

Extremely shady bank Wells Fargo and “Don’t Call Me A Bank” bank Chime had something in common this week — was serving up shit sandwiches for at least some consumers.

Let’s start with Chime, who is catching flack for an unusually high number of complaints to the Consumer Financial Protection Bureau largely revolving around closed accounts and inaccessible cash. To hear Chime tell it, these shutdowns are a result of their fraud detection process, and stemming the tide of an “extraordinary surge in activity by those seeking to illicitly obtain pandemic-related government funds and defraud US taxpayers” and that they do give consumers an (infuriating, most likely) avenue to recover their funds.

Marketing aside, Chime is, in fact, not a bank and is responsible to its other clients — Stride and Bancorp, the sponsor banks from whom Chime is effectively renting a bank license — for compliance and fraud detection. They’re making sure they play it safe on that front. Chime pioneered some cool features like Earned Wage Access (get your direct deposit two days early), and has led the charge in the slow erosion of predatory overdraft fees, but every so often, you can feel the seams of Chime not having its own license. For example, sometimes there are extremely long delays in ACH deposits from other institutions reaching your account. These closures feel somewhat related to that issue, and possibly explain why Chime is such an outlier on complaints in comparison to something like Marcus by Goldman which does have its own license.

Never to be outdone, Wells Fargo is making people angry again. In a move in line with a recurring theme of shedding various credit and lending products, Wells is shutting down all existing personal lines of credit. The disclosure that shutting down these credit lines “may have an impact on your credit score” has folks justifiably mad, and there’s no real excuse other than “operations are tight following our massive fake account scandal” that will surely keep affecting the bank for years to come.

While this overall probably won’t really kill anyone’s credit, with a little bit of bad timing, suddenly removing an available line of credit while at the same time increasing your credit utilization can and will hurt some consumers. That says at least as much about our silly credit scoring system as it does Wells Fargo, but “help” might be on the way.

Be careful what you wish for (*monkey’s paw curls*).

Binance Family Adventure

Crypto exchange facing Increased regulatory scrutiny

Lastly, I’m sure someone will write the deep dive on Binance’s recent legal troubles, but I just want to focus on my favorite quote of the week: “compliance is a journey” from renegade CEO Changpeng “CZ” Zhao in an open letter to the series of regulators around the world around the world amid increasing scrutiny into the world’s largest cryptocurrency exchange.

{kind=link}

Binance’s issues generally stem from the fact that they are not regulated or licensed in many of the countries their users trade from, and haven’t shown any inclination to become so. It’s certainly a contrasting approach to compliance-first organizations like Coinbase and Gemini, and they are fairly adept at using an expansive corporate structure to avoid having to deal with those pesky regulators. In some jurisdictions, like the US, they have spun up “fully independent” “brand partnership” entities like Binance.US which are licensed and regulated (and have far fewer features than main-line Binance).

The FCA (UK regulatory authority) has taken notice and announced that one of Binance’s many affiliates “is not permitted to undertake any regulated activity in the UK.” This has caused a cascade of issues, including European banking giants Barclays and Santander blocking payments to the exchange. The hits are starting to pile up, hence the open letter.

For what it’s worth, Binance at least seems ready to start making the transition to playing nice with regulators, lest they start needing to spin up “fully independent” subsidiaries in every country. Even Binance.US is now led by former Acting Controller of Currency and former Coinbase CLO Brian Brooks. Eventually you reach the “ask for forgiveness” period of the move-fast-and-break-things lifecycle and it seems like we’re there for Binance.

And to be fair “compliance is a journey, not a destination” is a somewhat common phrase, but it’s very amusing in this context where the problem is Binance wasn’t on journey in the first place. Maintaining compliance might be a journey, but only once you’ve actually attempted to achieve some level of it. Until then, compliance is a negotiation. One you have with your product team, your sales team, operations, legal, and most importantly with regulators. Binance can look at the example from AngelList as it starts discussions, or CZ can reach out to IF:Then — we are here to help.

Until next week, friends - David Ikenna Adams

If you liked this content and want to hear more every Sunday, please subscribe. If you’d like to join the IF:Then community, please reach out to me david@ifthen.vc